Data Management

Tech

.png)

Aug 7, 2025

4 minutes

In lending technology, LOS (Loan Origination System) and LMS (Loan Management System) serve different but connected functions. While both are essential to the lifecycle of a loan operationally, they address distinct stages of the credit process - with different data models, workflows, and user needs.

This article breaks down the key differences between LOS and LMS, where they intersect, and why private credit teams often need both - or a tightly integrated alternative.

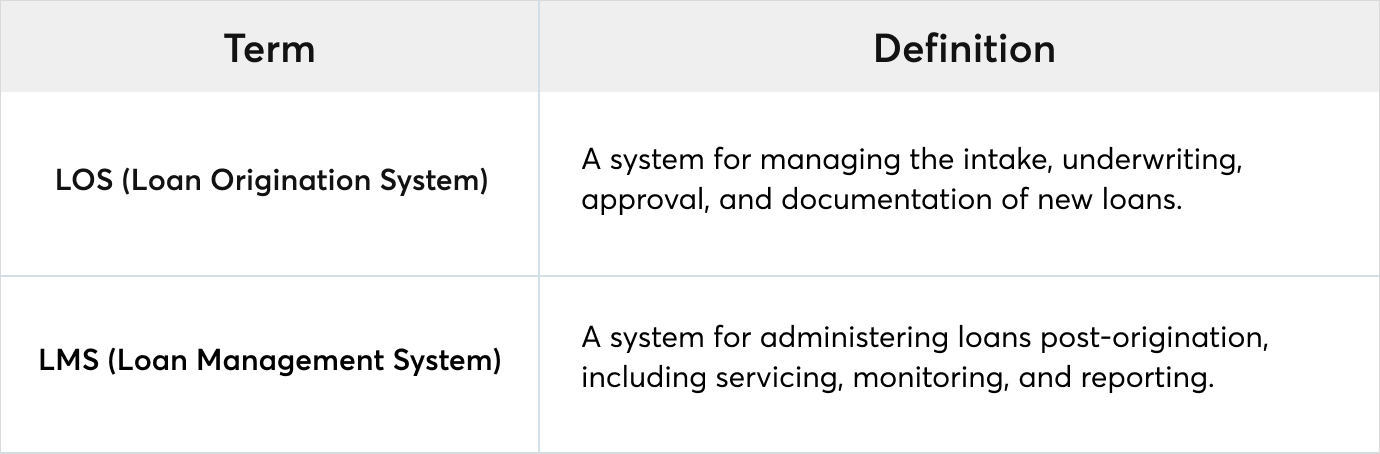

A Loan Origination System (LOS) handles the front end of the credit process - borrower intake, underwriting, term structuring, and approvals. It defines key elements like principal, rates, fees, and covenants.

Once the loan is signed and funded, the Loan Management System (LMS) takes over - applying those terms in practice. It tracks payments, manages schedules, handles changes, and supports investor and portfolio reporting.

In short: LOS structures the deal. LMS makes it run.

LOS focuses on:

LMS focuses on:

In private credit, the line between LOS and LMS is increasingly blurred. Loans rarely follow a clean, linear lifecycle - drawdowns are dynamic, amendments are frequent, and the same team often manages both origination and servicing. As a result, credit teams need systems that don’t just hand off between stages, but unify them.

Traditionally, a Loan Origination System (LOS) is used by front-office teams to structure and approve deals. It manages intake, underwriting, documentation, and internal workflows. The Loan Management System (LMS) takes over post-funding - handling repayments, changes, reporting, and investor communications.

But in practice, these systems rely on shared data: terms, entities, tranche rules, covenants, and funding logic. Without a seamless connection, teams face manual rework, misalignment, and operational risk.

Some platforms bridge this gap with integrations or internal tools. Others offer both LOS and LMS functionality in a single platform. But the ideal scenario is a system that doesn’t just receive data - it starts at deal structuring and carries through to repayment and reporting.

A modern LMS needs to do more than service a loan. It should also support origination logic: mapping legal and funding entities, capturing bespoke terms, setting up tranche participation, and running simulations before funding. Especially for private credit funds that structure in-house or operate without a dedicated LOS, this level of control is essential.

When origination and servicing live in separate systems, managing that complexity becomes harder. Terms need to be re-entered, payment logic gets rebuilt from scratch, and amendments can drift from what was originally agreed. These gaps introduce real operational risk - from misapplied payments to investor reporting errors and audit challenges.

This fragmentation also slows teams down. It makes automation harder, reporting less reliable, and internal controls harder to enforce - especially in regulated environments.

That’s why more credit funds are moving toward unified systems that support the full loan lifecycle. When origination flows directly into servicing, teams can maintain accuracy, enforce consistency, and scale with confidence.

At Hypercore, we’ve built our platform to reflect this reality - supporting both origination logic and post-close operations in one place, so credit teams can stay in sync from the start of the deal to the final repayment.

AI

Thought Leadership

May 19, 2026