Data Management

Thought Leadership

Dec 1, 2025

3 minutes

The primary risk threatening modern credit funds is not a market downturn, but operational failure - a crisis often masked by the deceptive familiarity of spreadsheets. This is the Spreadsheet Stockholm Syndrome: the bias causing fund operations to cling to fragile Excel models for mission-critical loan ervicing, portfolio management, and risk modeling. This reliance transforms operational inefficiency into systemic regulatory exposure and unmanaged default risk, directly compromising NAV integrity. For any fund committed to scalable growth and robust governance, the solution requires a dedicated custom Loan Management Platform and the decisive leadership to implement the non-negotiable strategy: Burn the Boats.

In private credit, the greatest threat is rarely market volatility - it is operational failure.

Despite sophisticated portfolios, many funds still run mission-critical tasks through massive spreadsheet ecosystems:

This creates an illusion of control. Teams trust the spreadsheet because they built it, but this human-centric process is precisely what introduces systemic operational risk.

For this article's purposes, Spreadsheet Stockholm Syndrome is the organizational attachment to complex spreadsheets for mission-critical loan servicing, portfolio management, and operational workflows, despite the risk of:

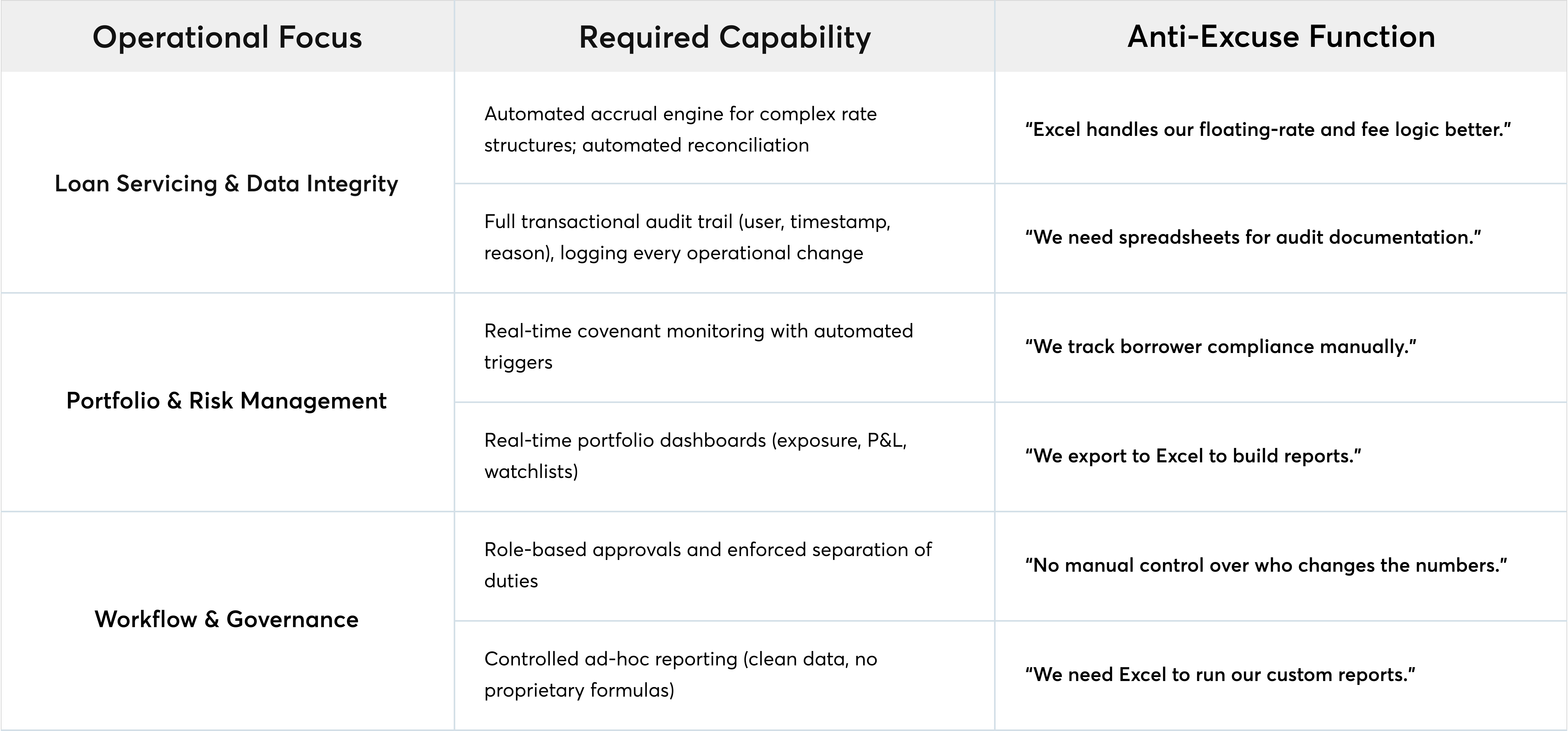

1. Loan Servicing and Reconciliation Failure (Direct P&L Leakage)

2. Covenant Monitoring Gaps (Avoidable Default Risk)

3. Audit, Compliance, and Governance Failures (The Regulatory Trap)

The solution is not patching spreadsheets, it is replacing the entire manual layer with a purpose-built Loan Management System (LMS).

Keeping operational spreadsheets running after implementing a loan management system creates:

Burn the Boats means:

✔ Decommissioning all mission-critical servicing and portfolio spreadsheets

✔ Enforcing the platform as the Single Source of Truth (SSOT)

✔ Eliminating the possibility of operational backsliding

✔ Ensuring full user adoption across the fund

Below are the critical features that eliminate every excuse to revert to spreadsheets.

Spreadsheet dependence isn’t just inefficient, it’s a structural risk that grows with every new facility, amendment, and reporting cycle. Credit funds that replace manual processes with a purpose-built loan management system gain something Excel can’t provide: consistent logic, auditability, and a single, defensible source of truth. Once servicing, covenants, and reporting run inside an enforceable workflow, teams stop firefighting and start scaling. In today’s environment, operational reliability isn’t optional, it’s the foundation that protects performance, integrity, and investor trust.

AI

Thought Leadership

Jul 31, 2026

.png)

.png)