Roadmap

Tech

Nov 13, 2025

4 minutes

Private credit funds enter 2026 with rising operational complexity and new expectations around scale, controls, reporting, and automation. This article outlines a practical, actionable technology roadmap to help managers modernize infrastructure and achieve durable operational advantage.

Private credit funds are entering 2026 with unprecedented demands for scale, cleaner data, audit-ready workflows, and faster decision-making.

Technology delivers the highest leverage when it centralizes data, automates recurring tasks, and provides real-time visibility across the entire portfolio.

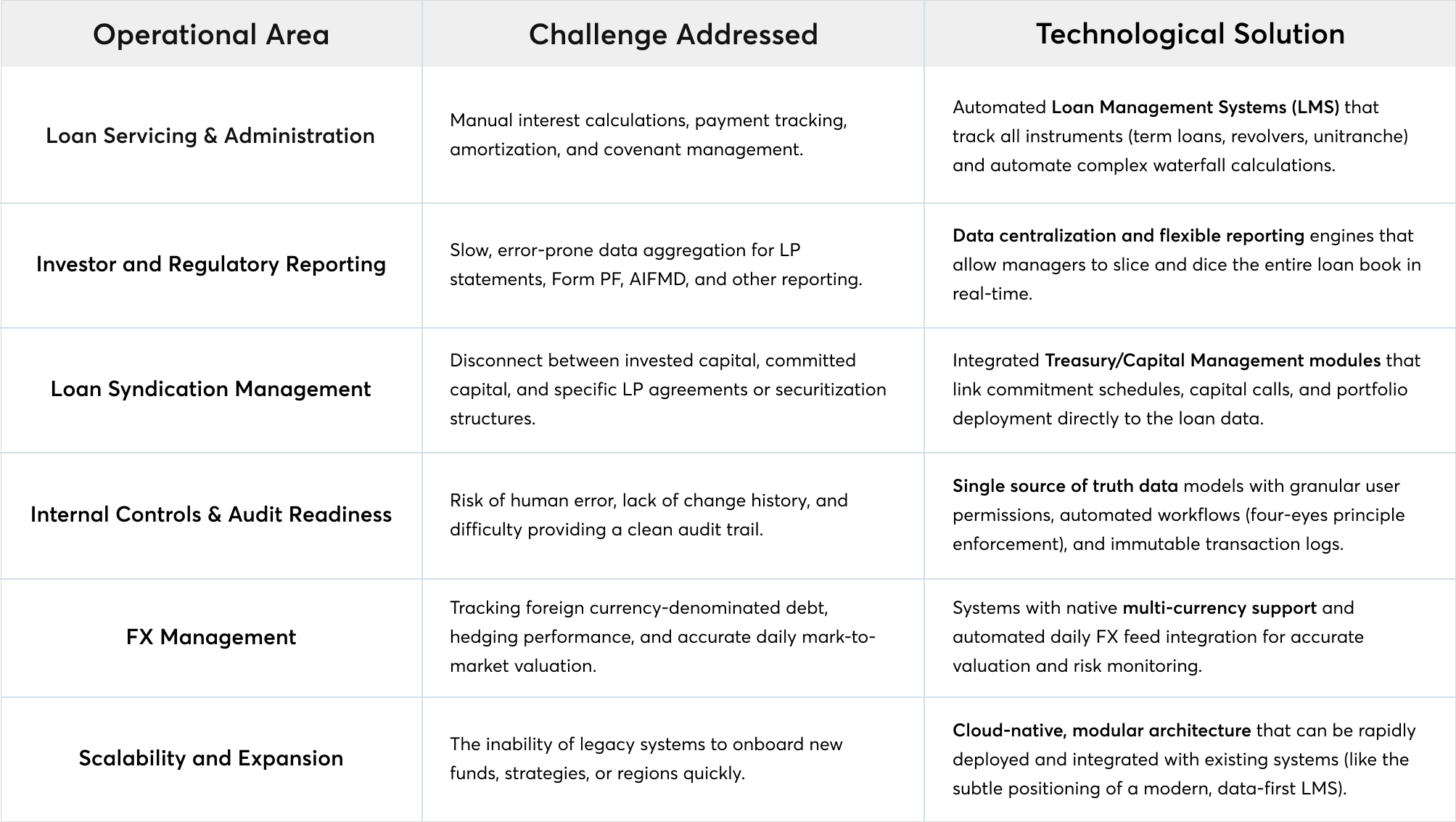

The most significant gains are found in the following core areas:

Private credit fund managers should evaluate their current technology stack based on its ability to:

The latest evolution of artificial intelligence moves beyond predictive analytics to autonomous AI agents, systems empowered to execute actions based on pre-defined triggers and permissions. Operating directly atop the clean, centralized data infrastructure of a modern Loan Management System (LMS), these agents are the ultimate form of operational leverage, enabling platforms to run key workflows with near-zero latency and minimal human intervention.

These autonomous agents can be deployed across high-value operational areas. For instance, a Covenant Compliance Agent continuously monitors real-time borrower financials; upon detecting a potential breach, it instantly flags the loan officer, generates an internal report, and initiates a formal "Watchlist" workflow. Similarly, a Capital Call & Distribution Agent uses commitment data to calculate and execute capital calls or distributions, automatically drafting notices and initiating fund transfers via API integration, all while adhering to pre-defined risk and control parameters.

Crucially, the success of execution agents depends entirely on the underlying data foundation. Implementation requires three non-negotiable prerequisites: (1) A Single Source of Truth (the LMS) for structured, validated data; (2) API Connectivity for communication with external systems (banks, GL) to execute actions; and (3) Strict Internal Controls that define the agent's authority and maintain an immutable audit trail for every action performed. This move to autonomous execution is the differentiator for private credit funds seeking scalable, error-proof operations in 2026.

Step 1 - Centralize your data into a single LMS

A unified source of truth underpins scale, auditability, and AI readiness.

Step 2 - Automate core servicing workflows

Replace spreadsheets with automated amortization, interest calculations, and reconciliations.

Step 3 - Implement internal controls and approval layers

Enforce segregation of duties, draft–review–approval, and tamper-proof audit logs.

Step 4 - Integrate upstream and downstream systems

Use APIs to connect the LMS to banking, GL, CRM, data providers, and investor portals.

Step 5 - Deploy AI agents for high-volume operational tasks

Start with borrower data ingestion, covenant checks, amendments, and reporting workflows.

Step 6 - Expand into capital activity and cross-entity automation

Once the core is stable, automate capital calls, distributions, and multi-vehicle reporting.

As private credit managers close out 2025 and strategically plan for 2026, the mandate is clear: technology is the new infrastructure of alpha. Continued reliance on legacy systems and manual workarounds is not only a constraint on growth but a significant source of operational risk.

Leaders must prioritize the implementation of a modern, cloud-native Loan Management System that centralizes data, automates core servicing, and provides the API connectivity required to build a resilient, scalable, and data-driven platform. The successful private credit fund of 2026 will be the one that has strategically invested in technology to transform operational friction into a competitive advantage and position itself to lead the next phase of market growth.

The most successful private credit platforms in 2026 will be those that modernize their operational core and treat technology not as an accessory, but as the infrastructure of scale.

AI

Thought Leadership

May 19, 2026